Accounting according to the Czech legislation or IFRS? Czechia case study

DOI: https://doi.org/10.3846/jbem.2024.21531Abstract

The article deals with the decision-making situation whether it is more advantageous for accounting entities in Czechia to keep accounting according to Czech accounting regulations or to International Financial Reporting Standards. The preparation of financial statements only in accordance with national accounting regulations may often not be sufficient. Different ways of regulating accounting in the world put pressure on accounting harmonization. International Financial Reporting Standards are the world’s primary tools for accounting harmonization. The results of the decision analysis show that it is more advantageous for accounting entities to prepare financial statements only in accordance with national accounting regulations. The main reason for the higher utility of this option is lower costs, which is the most important criterion in the decision-making process. While accounting entities confirm that the preparation of financial statements in accordance with International Financial Reporting Standards provides higher quality and comparability of accounting information, it also provides higher costs. In the article are used methods of analysis, synthesis, comparison and a selected method of multi-criteria decision making.

Keywords:

accounting, analytic hierarchy process, Czechia, financial statements, international financial reporting standards, harmonization of accountingHow to Cite

Share

License

Copyright (c) 2024 The Author(s). Published by Vilnius Gediminas Technical University.

This work is licensed under a Creative Commons Attribution 4.0 International License.

References

Ahmed, A. S., Neel, M., & Wang, D. (2013). Does mandatory adoption of IFRS improve accounting quality? Preliminary evidence. Contemporary Accounting Research, 30(4), 1344–1372. https://doi.org/10.1111/j.1911-3846.2012.01193.x> https://doi.org/10.1111/j.1911-3846.2012.01193.x

Akamash, H., Marson, S., & Shafron, E. (2022). Disincentives to exchange customized local GAAP for IFRS. Journal of Accounting and Public Policy, 41(6), Article 107002. https://doi.org/10.1016/j.jaccpubpol.2022.107002> https://doi.org/10.1016/j.jaccpubpol.2022.107002

Anaga, J., Zori, G., & Alon, A. (2023). IFRS adoption approaches and accounting quality. International Journal of Accounting, 58(3). https://doi.org/10.1142/S1094406023500099> https://doi.org/10.1142/S1094406023500099

Andrejovská, A., Konečná, V., & Hakalová, J. (2020). Tax gap as a tool for measuring VAT evasion in the EU countries. Ad Alta-Journal of Interdisciplinary Research, 10(2), 8–13. https://doi.org/10.33543/1002813> https://doi.org/10.33543/1002813

Azzali, S., Mazza, T., Reichelt, K., & Wang, D. (2021). Does mandatory IFRS adoption affect audit hours and the effectiveness to constrain earnings management? Evidence from Italy. Auditing – A Journal, of Practice & Theory, 40(4), 1–25. https://doi.org/10.2308/AJPT-18-061> https://doi.org/10.2308/AJPT-18-061

Barth, M. (2022). Accounting standards: The ‘too difficult’ box – the next big accounting issue? Accounting and Business Research, 52(5), 565–577. https://doi.org/10.1080/00014788.2022.2079757> https://doi.org/10.1080/00014788.2022.2079757

Bassemir, M., & Novotny-Farkas, Z. (2018). IFRS adoption, reporting incentives and financial reporting quality in private firms. Journal of Business Finance & Accounting, 45(7–8), 759–796. https://doi.org/10.1111/jbfa.12315> https://doi.org/10.1111/jbfa.12315

Baudot, L., Demek, K. C., & Huang, Z. (2018). The accounting profession’s engagement with accounting standards: Conceptualizing accounting complexity through big 4 comment letters. Auditing: A Journal of Practice & Theory, 37(2), 175–196. https://doi.org/10.2308/ajpt-51898> https://doi.org/10.2308/ajpt-51898

Byard, D., Li, Y., & Yu, Y. (2011). The effect of mandatory IFRS adoption on financial analysts information environment. Journal of Accounting Research, 49(1), 69–96. https://doi.org/10.1111/j.1475-679X.2010.00390.x> https://doi.org/10.1111/j.1475-679X.2010.00390.x

Cipriano, M., Cole, E., & Briggs, J. (2022). Value relevance and market valuation of assets measured using IFRS and US GAAP in the US equity market. International Journal of Accounting and Information Management, 30(1), 95–114. https://doi.org/10.1108/IJAIM-06-2021-0126> https://doi.org/10.1108/IJAIM-06-2021-0126

Chačiev, G. (2016, September 21). Portrét ČR z pohledu zahraničního experta [Portrait of the Czech Republic from the perspective of a foreign expert]. Statistika & my. https://www.statistikaamy.cz/2016/10/21/portret-cr-z-pohledu-zahranicniho-experta/> https://www.statistikaamy.cz/2016/10/21/portret-cr-z-pohledu-zahranicniho-experta/

Chamber of Auditors of the Czech Republic. (n.d.). Mezinárodní auditorský standard ISA 530 „Výběr vzorků a další způsoby testování“. Retrieved November 1, 2022, from https://www.kacr.cz/data/Metodika/Auditing/ISA/ISA530.pdf> https://www.kacr.cz/data/Metodika/Auditing/ISA/ISA530.pdf

Cho, M., Kim, S., Kim, Y., Lee, B. B. H., & Lee, W. (2021). IFRS adoption and stock misvaluation: Implication to Korea discount. Research in International Business Finance, 58, Article 101494. https://doi.org/10.1016/j.ribaf.2021.101494> https://doi.org/10.1016/j.ribaf.2021.101494

Cui, L., Kent, P., Kim, S., & Li, S. (2021). Accounting conservatism and firm performance during the COVID-19 pandemic. Accounting and Finance, 61(4), 5543–5579. https://doi.org/10.1111/acfi.12767> https://doi.org/10.1111/acfi.12767

Czech Statistical Office. (n.d.). Hlavní makroekonomické ukazatel [Key macroeconomic indicators]. Retrieved April 1, 2023, from https://www.czso.cz/csu/czso/hmu_cr> https://www.czso.cz/csu/czso/hmu_cr

Czech Statistical Office. (2022). Statistická ročenka České republiky – 2022 [Statistical yearbook of the Czech Republic – 2022]. https://www.czso.cz/csu/czso/statisticka-rocenka-ceske-republiky-2022> https://www.czso.cz/csu/czso/statisticka-rocenka-ceske-republiky-2022

Da Silva, A., J. Brighenti, J., Klann, R. C. (2018). Effects of convergence on international accounting standards on the relevance of accounting information of Brazilian companies. Revista Ambiente Contabil, 10(1), 121–138.

Dhallwal, D., He, W., Li, Y., & Pereira, R. (2019). Accounting standards harmonization and financial integration. Contemporary Accounting Research, 36(4), 2437–2466. https://doi.org/10.1111/1911-3846.12495> https://doi.org/10.1111/1911-3846.12495

Duan, X. (2016). Accounting information fusion for decision making. In C. Foo (Ed.), Diversity of managerial perspectives from inside China (pp. 67–81). Springer. https://doi.org/10.1007/978-981-287-555-6_5> https://doi.org/10.1007/978-981-287-555-6_5

Edeigba, J., Gan, S., & Amenkhienan, S. (2020). The influence of cultural diversity on the convergence of IFRS: Evidence from Nigeria IFRS implementation. Review of Quantitative Finance and Accounting, 55(1), 105–121. https://doi.org/10.1007/s11156-019-00837-0> https://doi.org/10.1007/s11156-019-00837-0

Efretuei, E., Usoro, A., & Koutra, C. (2022). Complex information and accounting standards: Evidence from UK narrative reporting. South African Journal of Accounting Research, 36(3), 171–194. https://doi.org/10.1080/10291954.2021.1970450> https://doi.org/10.1080/10291954.2021.1970450

Encarnacion, V. (2022). A model proposal based on IFRS SMEs for the improvement of economic and financial management in small enterprises in Guayaquil. Revista Finanzas Politica Economica, 14(1), 49–74. https://doi.org/10.14718/revfinanzpolitecon.v14.n1.2022.3> https://doi.org/10.14718/revfinanzpolitecon.v14.n1.2022.3

Fernandez, G., Willa, V., Cepeda, O., Flores, R., & Nina, D. (2019). The international financial reporting standards (IFRS) and its application in SMEs in Ecuador. Revista Inclusiones, 6, 331–351.

Gambie, J. (2022). ‘Occupation’, labour markets and qualification futures. Journal of Vocational Education and Training, 74(2), 311–332. https://doi.org/10.1080/13636820.2020.1760336> https://doi.org/10.1080/13636820.2020.1760336

Hartmann, B., Marton, J., & Sols, J. (2020). IFRS in national regulatory space: Insights from Sweden. Accounting in Europe, 17(3), 367–387. https://doi.org/10.1080/17449480.2020.1824073> https://doi.org/10.1080/17449480.2020.1824073

Haiduchenko, S., Lelechenko, A., Dobryn, S., & Kipa, M. (2020). Mechanism of management of financial resources of enterprises of the machine-building industry of Ukraine. Financial and Credit Activities: Problems of Theory and Practice, 1(32), 87–99. https://doi.org/10.18371/fcaptp.v1i32.200291> https://doi.org/10.18371/fcaptp.v1i32.200291

Homola, D., & Pasekova, M. (2020). Factors influencing true and fair view when preparing financial statements under IFRS: Evidence from the Czech Republic. Equilibrium-Quarterly Journal of Economics and Economic Policy, 15(3), 595–611. https://doi.org/10.24136/eq.2020.026> https://doi.org/10.24136/eq.2020.026

Informační systém o průmerne výdĕlku. (2023). Aktuální výsledky šetření [Current results of the survey]. https://www.ispv.cz/cz/Vysledky-setreni/Aktualni.aspx> https://www.ispv.cz/cz/Vysledky-setreni/Aktualni.aspx

Jindřichovská, I., & Kubíčková, D. (2017). The role and current status of IFRS in the completion of national accounting rules – Evidence from the Czech Republic. Accounting in Europe, 14(1–2), 56–66. https://doi.org/10.1080/17449480.2017.1301671> https://doi.org/10.1080/17449480.2017.1301671

Kainth, A., & Wahlstrom, R. (2021). Do IFRS promote transparency? Evidence from the bankruptcy prediction of privately held Swedish and Norwegian companies. Journal of Risk and Financial Management, 14(3), Article 123. https://doi.org/10.3390/jrfm14030123> https://doi.org/10.3390/jrfm14030123

Karban, P. (2020). Zpráva o českych krajích 2020. Rozdíly mezi regiony přetrvávají [Report on Czech Regions 2020. Differences between regions persist]. Czech Chamber of Commerce. Businessinfo.cz. https://www.businessinfo.cz/clanky/zprava-o-ceskych-krajich-2020-rozdily-mezi-regiony-pretrvavaji/> https://www.businessinfo.cz/clanky/zprava-o-ceskych-krajich-2020-rozdily-mezi-regiony-pretrvavaji/

Khan, S., Abdou, K., & Ghosh, S. (2020). Mandatory adoption of IFRS and its effect on international stock listings in Canada. Journal of Financial Regulation and Compliance, 28(3), 409–429. https://doi.org/10.1108/JFRC-01-2020-0010> https://doi.org/10.1108/JFRC-01-2020-0010

Kissell, R. (2021). Machine learning techniques. In Algorithmic trading methods: Applications using advanced statistics, optimization, and machine learning techniques (pp. 221–231). Elsevier. https://doi.org/10.1016/B978-0-12-815630-8.00009-0> https://doi.org/10.1016/B978-0-12-815630-8.00009-0

Krajňák, M. (2020). Financial statement according to national or international financial reporting standards? A decision analysis case study from the Czech Republic at industrial companies. Inzinerine Ekonomika-Engineering Economics, 31(3), 270–281. https://doi.org/10.5755/j01.ee.31.3.22715> https://doi.org/10.5755/j01.ee.31.3.22715

Krzikallova, K., & Tosenovsky, F. (2020). Is the value added tax system sustainable? The case of the Czech and Slovak Republics. Sustainability, 12(12), Article 4925. https://doi.org/10.3390/su12124925> https://doi.org/10.3390/su12124925

Kubota, T., & Okuda, S. (2023). Relationship between top managers’ interest in accounting information and accounting practices in startups. International Journal of Accounting Information Systems, 51, Article 100640. https://doi.org/10.1016/j.accinf.2023.100640> https://doi.org/10.1016/j.accinf.2023.100640

Kulakowski, K. (2020). Understanding the analytic hierarchy process. Routledge. https://doi.org/10.1201/b21817> https://doi.org/10.1201/b21817

Li, D., Lim, Y., & Morris, R. (2022). The impact of IFRS on the use of private debt covenants international evidence. Journal of International Accounting Research, 21(2), 125–150. https://doi.org/10.2308/JIAR-2021-085> https://doi.org/10.2308/JIAR-2021-085

Li, F., Xie, L., & Ruan, Y. (2023). Tax-cut policies, accounting conservatism, and corporate tax burden stickiness: Empirical analysis from China. Journal of Tax Reform, 9(2), 197–216. https://doi.org/10.15826/jtr.2023.9.2.137> https://doi.org/10.15826/jtr.2023.9.2.137

Lin, S., Riccardi, W., & Wang, C. (2019). Relative effects of IFRS adoption and IFRS convergence on financial statement comparability. Contemporary Accounting Research, 36(2), 588–617. https://doi.org/10.1111/1911-3846.12475> https://doi.org/10.1111/1911-3846.12475

Matthews, K. (2021). Consequences of labor cost reduction practices: A structured literature review. Accounting Perspectives, 20(4), 687–718. https://doi.org/10.1111/1911-3838.12276> https://doi.org/10.1111/1911-3838.12276

Mhedhbi, K., & M. Essid, M. (2022). National cultural dimensions and adoption of the international financial reporting standard (IFRS) for small and medium-sized entities (SMEs). International Journal of Accounting, 57(1), Article 22500044. https://doi.org/10.1142/S1094406022500044> https://doi.org/10.1142/S1094406022500044

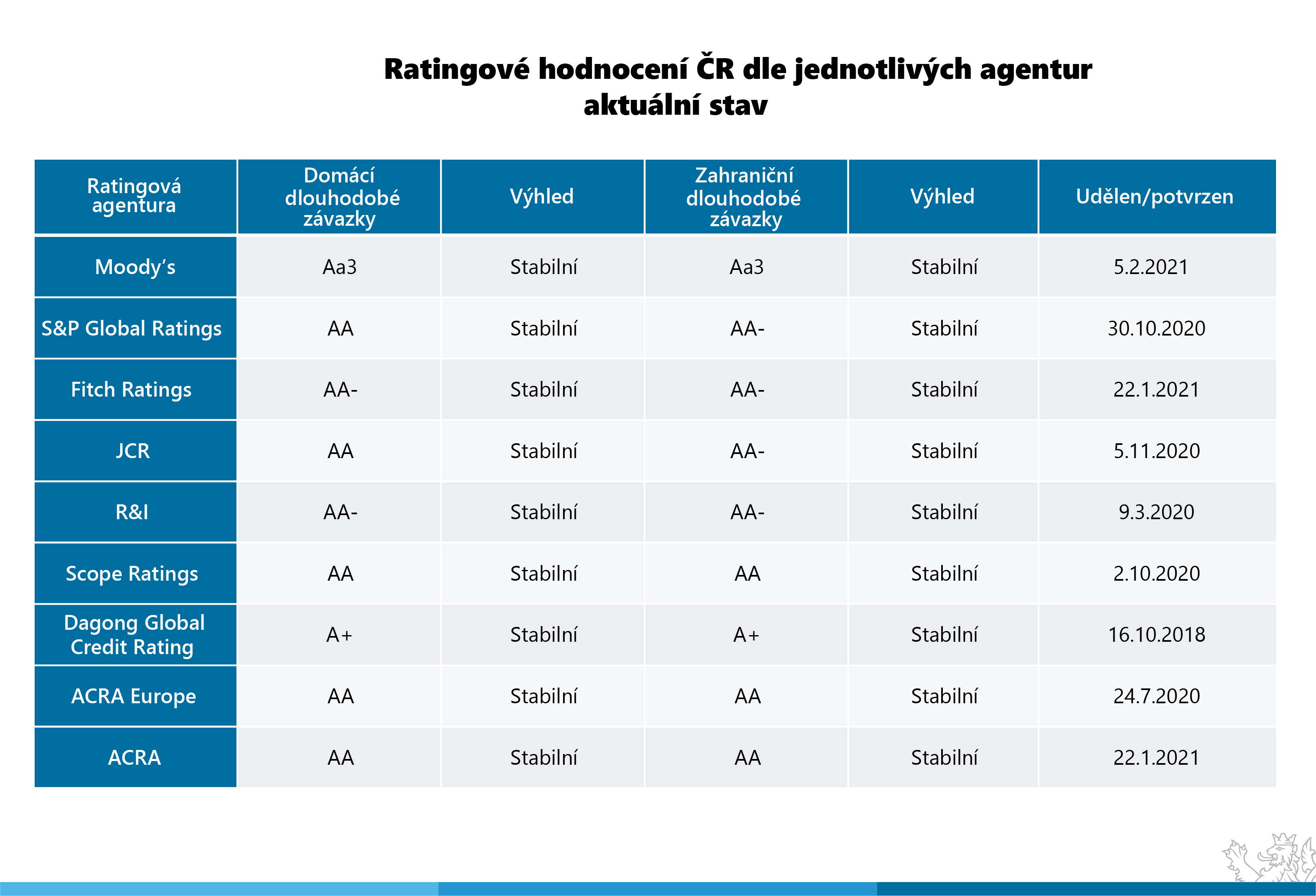

Ministry of Finance of the Czech Republic. (2021). Ratingové hodnocení ČR dle jednotlivých agentur aktuální stav [Rating of the Czech Republic by individual agencies current status]. https://www.mfcr.cz/assets/cs/media/2021-02-05_Ratingove-hodnoceni-CR-dle-jednotlivych-agentur.png> https://www.mfcr.cz/assets/cs/media/2021-02-05_Ratingove-hodnoceni-CR-dle-jednotlivych-agentur.png

{kind=link}

Moore, D. (2020). Statistics: Concepts and controversies (10th ed.). Macmillan.

Na, W. (2011). Research on the application and development prospects of accounting. In M. Dai (Ed.), Innovative computing and information: Vol. 231. Communications in computer and information science (pp. 233–237). Springer. https://doi.org/10.1007/978-3-642-23993-9_34> https://doi.org/10.1007/978-3-642-23993-9_34

Nam, J., & Thomson, R. (2023). Does financial statement comparability facilitate SEC oversight? Contemporary Accounting Research, 40(2), 1315–1349. https://doi.org/10.1111/1911-3846.12835> https://doi.org/10.1111/1911-3846.12835

Neisen, M., & Schulte-Mattler, H. (2021). The effectiveness of IFRS 9 transitional provisions in limiting the potential impact of COVID-19 on banks. Journal of Banking Regulation, 22, 342–351. https://doi.org/10.1057/s41261-021-00151-7> https://doi.org/10.1057/s41261-021-00151-7

Nobes, C., & Zeff, A. (2016). Have Canada, Japan and Switzerland adopted IFRS? Australian Accounting Review, 26(3), 284–290. https://doi.org/10.1111/auar.12131> https://doi.org/10.1111/auar.12131

Obradović, V., Čupić, M., & Dimitrijević, D. (2018). Application of international financial reporting standards in the transition economy of Serbia. Australian Accounting Review, 28(1), 48–60. https://doi.org/10.1111/auar.12187> https://doi.org/10.1111/auar.12187

Opare, S., Houque, M., & Zijil, T. (2021). Meta-analysis of the impact of adoption of IFRS on financial reporting comparability, market liquidity, and cost of capital. Abacus – A Journal of Accounting Finance and Business Studies, 57(3), 502–556. https://doi.org/10.1111/abac.12237> https://doi.org/10.1111/abac.12237

Owais, W. A., & Dahiyat, A. A. (2021). Readiness and challenges for applying IFRS 17 (insurance contracts): The case of Jordanian insurance companies. Journal of Asian Finance Economics and Business, 8(3), 277–286. https://doi.org/10.13106/jafeb.2021.vol8.no3.0277> https://doi.org/10.13106/jafeb.2021.vol8.no3.0277

Paseková, M., Kramná, E., Svitáková, B., & Dolejšová, M. (2019). Relationship between legislation and accounting errors from the point of view of business representatives in the Czech Republic. Oeconomia Copernicana, 10(1), 193–210. https://doi.org/10.24136/oc.2019.010> https://doi.org/10.24136/oc.2019.010

Pavlatos, O. (2021). The impact of economic crisis on cost structure configuration. Economics and Business Letters, 10(1), 87–94. https://doi.org/10.17811/ebl.10.1.2021> https://doi.org/10.17811/ebl.10.1.2021

Pawsey, N. (2017). IFRS adoption: A costly change that keeps on costing. Accounting Forum, 41(2), 116–131. https://doi.org/10.1016/j.accfor.2017.02.002> https://doi.org/10.1016/j.accfor.2017.02.002

Pechancová, V., Pavelková, D., & Saha, P. (2022). Community renewable energy in the Czech Republic: Value proposition perspective. Frontiers in Energy Research, 10. https://doi.org/10.3389/fenrg.2022.821706> https://doi.org/10.3389/fenrg.2022.821706

Pohoda. (n.d.). Ceník programu pohoda. https://www.stormware.cz/pohoda/cenik.aspx> https://www.stormware.cz/pohoda/cenik.aspx

Rosmianingrum, A., Mohammed, N. F., Bujang, I., & Leo, L. (2023). IFRS adoption, stock price synchronicity and firm-specific information in Indonesia stock market. Cogent Business & Management, 10(1), Article 2170520. https://doi.org/10.1080/23311975.2023.2170520> https://doi.org/10.1080/23311975.2023.2170520

Sanchez, F., Giner. B., & Gill-de-Albornos, B. (2023). The decision to present comparative financial statements in a mandatory IFRS adoption setting. Baltic Journal of Management, 18(3), 350–365. https://doi.org/10.1108/BJM-03-2022-0090> https://doi.org/10.1108/BJM-03-2022-0090

Soam, S. K., Rao, S., Yashavanth, B. S., Balasani, R., Rakesh, S., Marwaha, S., Kumar, P., & Agrawal, R. C. (2023). AHP analyser: A decision-making tool for prioritizing climate change mitigation options and forest management. Frontiers in Environmental Science, 10. https://doi.org/10.3389/fenvs.2022.1099996> https://doi.org/10.3389/fenvs.2022.1099996

Song, X., & Trimble, M. (2022). The historical and current status of global IFRS adoption: Obstacles and opportunities for researchers. International Journal of Accounting, 57(2), Article 22500019. https://doi.org/10.1142/S1094406022500019> https://doi.org/10.1142/S1094406022500019

Stofková, J., Krejnus, M., Stofková, K. R., Melega, P., & Binasova, V. (2022). Use of the analytic hierarchy process and selected methods in the managerial decision-making process in the context of sustainable development. Suistainability, 14(18), Article 11546. https://doi.org/10.3390/su141811546> https://doi.org/10.3390/su141811546

Tanchev, S. (2022). Determinants of the proportional income tax revenue: A comparative assessment of Russia and Bulgaria. Journal of Tax Reform, 8(1), 54–68. https://doi.org/10.15826/jtr.2022.8.1.108> https://doi.org/10.15826/jtr.2022.8.1.108

Vox. (n.d.). International accounting standards. Retrieved January 2, 2023 form https://vox.cz/kategorie/kurzy-a-seminare/danove-a-ucetni-kurzy/mezinarodni-ucetni-standardy/> https://vox.cz/kategorie/kurzy-a-seminare/danove-a-ucetni-kurzy/mezinarodni-ucetni-standardy/

Yaser Saleh, Q., Barakat Al-Nimer, M., & Abbadi, S. S. (2023). The quality of cost accounting systems in manufacturing firms: A literature review. Cogent Business & Management, 10(1). https://doi.org/10.1080/23311975.2023.2209980> https://doi.org/10.1080/23311975.2023.2209980

View article in other formats

CrossMark check

Published

Issue

Section

Copyright

Copyright (c) 2024 The Author(s). Published by Vilnius Gediminas Technical University.

License

This work is licensed under a Creative Commons Attribution 4.0 International License.